Questions that are important to the sales process-

How do you like to be communicated with?

- telephone

- text

- email

- visit

When will you be moving?

Why are you moving?

When was the last time you moved?

Why are you moving?

What is your current lifestyle? What do you do Socially?

Do you love or participate in sports, arts, religious activities, etc.

If you could have one thing in your new home that is amazing, what would it be?

What is more important to you getting the most for your home or selling it quickly?

What was your past experience with a Realtor like?

What type of school does your child attend?

Do you require Financing?

Are you pre approved for financing? How much?

Use. always, open ended questions. in other words, questions that require an answer other than Yes and No!

Monday, April 14, 2014

Marketing To Generation X and Generation i

Who says we are all the same?

With each generation comes a new and vibrant personality. No longer is multigenerational marketing the most effective way to market to your clients. Each generation has its own method of communicating and must be addressed to suit the unique way they wish to be addressed.

Traditionalists like to read the newspaper. Today their newspaper is the internet as the "Greatest Generation" tackle contemporary media to address their need for information. They still enjoy communication by mail and telephone. However to cross the generational gap, internet communication is now an accepted manner to talk to one another.

Baby Boomers, born from 1946 to 1964 are influential due to their sheer size today. Their community is an important aspect of their existence. They, like the Traditionalist love to talk real estate. They love to own real estate. They love to collect real estate! Vacation properties, time shares, second homes, cottages and other investment properties are their love.

Baby Boomers love to talk. They talk on the phone. They gab on the cell phone. They even talk in long wordy emails and blogs.

Generation X is the Latch Key Generation born between 1965 and 1976. in this short period of time society created an anomaly to their parents, kids who had to help themselves as their parent went to work. These are my kids, your kids.

This generation lived in a time when diverse was rampant and single parent homes were the norm. Thus they have delayed marrying, having children as they seek a real live-work balance. Unlike their parents they will not work until the job is done, they work along with the job.

Their careers will likely range from place to place ten or twelve times as they search for a better more fulfilling existence. Personal time is much more important that work time to Gen X.

Technology was a fact of life for Gen X. they were born into the internet, gaming on line, email and more importantly texting. From this generation came much of the techno communication stuff we use today such as Facebook and Myspace.

While Boomers and Traditionalists respond to Brand marketing. Generation X and Y prefer lifestyle marketing. Gen X does not respond to fear based marketing as seen on TV infomercials.

"Buy today before it is too late!" Doomsday marking will not work here!

They are independent, so micromanaging and indirect communication will undermine your relationship with Gen X.

Generation Y, born from 1977 to 1994 is a whole different environment. This is the most educated generation ever. They are confident, fun, optimistic and collaborative. interestingly, they know how to get the correct answer but may not know how to calculate it. "Google it", they will say!

They love to do the right thing.

They have been told they are "Special". Remember the soccer leagues where everyone, even the losers got trophies! They were Generation Y! They have a unique sense of risk and consequences.

Again they do not respond well the brand marketing. They are motivated with money and success and are impatient and do not want to "pay their dues" to achieve success.

Gen Y want it now. Boomers believe you have to earn privileges, Gen Y want privilege now.

This trend has contributed to an important fact we are seeing among first time home buyers. Most young people are electing to stay at home or to rent in desirable areas. Since Gen Y is motivated highly by money, their first real estate purchase may be an investment property rather than a personal residence. In fact, aggressive Gen Y's are buying property in their teens and early twenties if they can get financing.

Gen Y love collaboration and lean on their peer group for advice. "Group think" pays volumes for them. It is imperative to not be the "expert" with Gen Y but to be a helper or influencer. They appreciate the knowledge and will make their own right decision. Let Gen Y navigate through their own direction towards the purchase.

Unlike Gen X who will confront on a moments notice, Gen Y is not confrontational. That is why texting is popular with this generation. They then have time to consider that response.

Generation X and Y are changing how we market. Less time is being spent by these generations at a computer and more is being spent on mobile. They need a condensed version of everything.

Gen Y are interactive. They co create and cooperate on projects. Thus a blog is imperative and must be included in your website. Social networking is a must as you develop trust socially and network collaboratively. Any social must be real and interactive to develop into trust and friendship. But Pinetrest is supplanting Facebook as these young entrepreneurs love picture statements rather than word essays.

On line activity is a must for GEN X and Y, but many like to remain lone wolf surfers, anonymous and social at the same time. Some of he most recent social sites show this character where you can identify single individuals that are close by without fear of retribution.

You must communicate their way. Text messaging is a must. They use a telephone only as a last resort.

So know the newest generations. They are our buyers and will soon be the dominant sellers on real estate as well.

With each generation comes a new and vibrant personality. No longer is multigenerational marketing the most effective way to market to your clients. Each generation has its own method of communicating and must be addressed to suit the unique way they wish to be addressed.

Traditionalists like to read the newspaper. Today their newspaper is the internet as the "Greatest Generation" tackle contemporary media to address their need for information. They still enjoy communication by mail and telephone. However to cross the generational gap, internet communication is now an accepted manner to talk to one another.

Baby Boomers, born from 1946 to 1964 are influential due to their sheer size today. Their community is an important aspect of their existence. They, like the Traditionalist love to talk real estate. They love to own real estate. They love to collect real estate! Vacation properties, time shares, second homes, cottages and other investment properties are their love.

Baby Boomers love to talk. They talk on the phone. They gab on the cell phone. They even talk in long wordy emails and blogs.

Generation X is the Latch Key Generation born between 1965 and 1976. in this short period of time society created an anomaly to their parents, kids who had to help themselves as their parent went to work. These are my kids, your kids.

This generation lived in a time when diverse was rampant and single parent homes were the norm. Thus they have delayed marrying, having children as they seek a real live-work balance. Unlike their parents they will not work until the job is done, they work along with the job.

Their careers will likely range from place to place ten or twelve times as they search for a better more fulfilling existence. Personal time is much more important that work time to Gen X.

Technology was a fact of life for Gen X. they were born into the internet, gaming on line, email and more importantly texting. From this generation came much of the techno communication stuff we use today such as Facebook and Myspace.

While Boomers and Traditionalists respond to Brand marketing. Generation X and Y prefer lifestyle marketing. Gen X does not respond to fear based marketing as seen on TV infomercials.

"Buy today before it is too late!" Doomsday marking will not work here!

They are independent, so micromanaging and indirect communication will undermine your relationship with Gen X.

Generation Y, born from 1977 to 1994 is a whole different environment. This is the most educated generation ever. They are confident, fun, optimistic and collaborative. interestingly, they know how to get the correct answer but may not know how to calculate it. "Google it", they will say!

They love to do the right thing.

They have been told they are "Special". Remember the soccer leagues where everyone, even the losers got trophies! They were Generation Y! They have a unique sense of risk and consequences.

Again they do not respond well the brand marketing. They are motivated with money and success and are impatient and do not want to "pay their dues" to achieve success.

Gen Y want it now. Boomers believe you have to earn privileges, Gen Y want privilege now.

This trend has contributed to an important fact we are seeing among first time home buyers. Most young people are electing to stay at home or to rent in desirable areas. Since Gen Y is motivated highly by money, their first real estate purchase may be an investment property rather than a personal residence. In fact, aggressive Gen Y's are buying property in their teens and early twenties if they can get financing.

Gen Y love collaboration and lean on their peer group for advice. "Group think" pays volumes for them. It is imperative to not be the "expert" with Gen Y but to be a helper or influencer. They appreciate the knowledge and will make their own right decision. Let Gen Y navigate through their own direction towards the purchase.

Unlike Gen X who will confront on a moments notice, Gen Y is not confrontational. That is why texting is popular with this generation. They then have time to consider that response.

Generation X and Y are changing how we market. Less time is being spent by these generations at a computer and more is being spent on mobile. They need a condensed version of everything.

Gen Y are interactive. They co create and cooperate on projects. Thus a blog is imperative and must be included in your website. Social networking is a must as you develop trust socially and network collaboratively. Any social must be real and interactive to develop into trust and friendship. But Pinetrest is supplanting Facebook as these young entrepreneurs love picture statements rather than word essays.

On line activity is a must for GEN X and Y, but many like to remain lone wolf surfers, anonymous and social at the same time. Some of he most recent social sites show this character where you can identify single individuals that are close by without fear of retribution.

You must communicate their way. Text messaging is a must. They use a telephone only as a last resort.

So know the newest generations. They are our buyers and will soon be the dominant sellers on real estate as well.

Monday, April 7, 2014

What CMHC increase really means

By Mark Weisleder, Lawyer

Also found in the Toronto Star

CMHC announced that it is raising their rates on mortgage insurance effective May 1, 2014, by an average of 15 per cent. Although this is not good news for homebuyers, it does not mean that the sky is falling either. Here's why:

If you are buying a home and have less than 20 per cent for the down payment, you need to obtain mortgage insurance, either through CMHC or a private insurance company such as Genworth Canada or Central Guaranty. The costs of the insurance are typically added to your mortgage and paid out over the 25 year amortized term.

The reason for mortgage insurance is that banks would likely not lend money to people who for example, only had saved 5 per cent for the down payment, unless the mortgage was insured. CMHC essentially guarantees the loan to the bank so that if the borrower defaults and the property is sold at a loss, CMHC pays the difference. CMHC claims that they need to raise the premiums so that they have more capital reserves in case more consumers default on their mortgages in the future.

For example, if you have a 5% down payment today and you wish to borrow $300,000, the cost for the mortgage insurance is 2.75% or $8,250. You do not pay for this up front. Instead, it gets added to your mortgage debt so you would borrow a total of $308,250 to net $300,000. Under the new rules, the rate would increase to 3.15%, or $9,410, so you would borrow a total of $309,410 to net the same $300,000.

If you took a 5 year mortgage at 3.49% interest today, your monthly payment would rise from $1,537 per month, to $1,543. This is an increase of $6 per month.

Some say that this could now make a home unaffordable for many first time buyers. I disagree. While no one likes any increase in costs, we are still in a historic period of extremely low interest rates. Compare this to 1990, when interest rates were 12 per cent. The same mortgage would cost you $3,193 per month. In 2008, when the interest rate was 7 per cent, the payment would have been $2,167 per month.

It seems that every day someone else comes out with a prediction on the future direction of house prices in Canada. For every bank economist who says that we will still see stable growth over the next few years, there are others who predict a soft landing, with perhaps a price correction of 2 to 3 per cent. And then others predict that we are headed for a major price crash of 20 per cent over the next 5 years. All I know is that we have seen a period of steady growth in the Canadian real estate market for the past 14 years, despite many earlier predictions of crashes. Canada remains one of the most stable places in the world to live and raise a family.

Buyers, the main message is that you do not have to rush out and buy a home to beat the May 1, 2014 date when the mortgage insurance rates go up. It is more important to just make sure you can afford the home you are interested in and that you properly inspect any home before you buy it.

Click here to read the article:

How to protect yourself in a bidding war

By Mark Weisleder, Lawyer

Also Found in the Toronto Star

The real estate markets are going a little crazy in Toronto and Vancouver, with out of control bidding wars, primarily for detached homes under 1 million dollars. Experts say it is because there is not enough supply. In some cases, over 20 offers are received and the successful buyers are paying sometimes tens or hundreds of thousands of dollars over the asking price. What's worse, many buyers are putting offers in without any conditions whatsoever, hoping this will sway the seller to accept their offer.

Buyers, you can still be protected in this scenario. Here's how:

Buyers should understand that in this environment, you are likely to lose up to 5 times before you win a bidding war. Still, it is important to remember that even if you make a bid without a condition, the home must be pre-inspected by a professional home inspector. This can get expensive, since the average home inspection report costs between $350 - $550, depending on the size of the home. As such, you may pay up to $2,500 in home inspection fees before you get an accepted offer. In my opinion, when buying a million dollar property, this is a worthwhile investment. I have heard too many stories of buyers who buy without an inspection, only to discover major problems after closing.

Before you get involved in this process, meet with a few different home inspectors to get an idea what they look for when inspecting a home. Then try to make a deal that if they end up doing multiple inspections for you, the costs will reduce on a per inspection basis. The main things to watch for are the age of the furnace, roof, water penetration issues and the electrical wiring. The inspector will also look for cracks, slopes in the floors and doors that do not close properly, which all could point to potential foundation issues.

I would also seriously consider backing out when there are more than 5 bidders on a home. You will likely have to seriously overpay to get the home, based on the irrationality of the other bidders. Even if you win, there may be problems with financing your purchase. Just because you may have qualified for a million dollar home, if your lender figures you paid too much, you will not get the loan you expected, which may result in your not being able to close your deal.

Some sellers have their own inspection done and make the report available to buyers. It is dangerous for a buyer to rely on this and not conduct their own inspection. These seller reports usually come with a disclaimer that they are for information purposes only and not a warranty so you won't be able to sue anyone after closing if the information turns out wrong, unless you can prove that the seller actively concealed major defects without telling you.

Foreigners continue to love Canadian real estate as it is seen as a safe haven. With the recent fall of the Canadian dollar, Canadian real estate just got 10 per cent cheaper for foreign investors. These people primarily buy condominiums, so don't expect a crash in the condominium market either.

When you are looking for a home, even at these prices, make sure you are close to public transit, and have nice amenities around you. You are not a stock day trader when you buy a home and then sell it shortly afterwards for a quick profit. If you are buying for the long term and can afford the payments, you do not have to worry about any future changes in the market or in interest rates.

Even when those around you are going crazy, be prepared and you can be successful, even in a bidding war.

Click here to read the article:

Protect your rental investment with a professional property manager

By Mark Weisleder, Lawyer

also found in Toronto Star

also found in Toronto Star

More and more Canadians are buying rental residential real estate for investment purposes. These properties offer in most cases, stable income that pays almost all expenses, with a real estate asset that will typically appreciate in value in the long term. However, there are many pitfalls with becoming a first time landlord. The good news is that with the assistance of a professional property manager, you can be protected and have peace of mind that your investment will be secure for the long term.

Here's why:

Tenants are properly screened

One of the toughest parts of owning a rental property is properly screening tenants in advance. If a mistake is made and the tenant stops paying rent and uses the system to delay, the owner will be faced with unpaid mortgage and other bills that could threaten their ownership. A property manager knows what information to look for and what questions to ask before renting out your unit, to assure that this does not occur. Problem tenants typically stay away when they see that a professional manager is reviewing all applications.

Rents are collected in a timely manner

Property managers generally have offices where it is easy for tenants to pay the rent, if they cannot pay by post-dated cheques or pre-authorized payments. You do not have to arrange to meet with the tenants at odd hours to collect rents. If rents are late, the property manager will likely start eviction proceedings to make sure that tenants get the message and pay the rent on time.

Repairs and Maintenance are attended to promptly

Do you really want a call at 11 pm that the furnace just broke down? With a property manager, all problems, 24/7, are directed to the property manager office. The property manager will have a list of approved contractors who can complete any repairs in a timely and cost-efficient manner, to keep both the landlord and the tenant happy. The property manager will also conduct routine maintenance checks to make sure that furnace filters, eavestroughs are cleaned in a timely manner, so that problems do not arise in the future. Sharon Golberg, President of Dash Property Management, www.dashpropertymanagement.com, which specializes in condominium properties downtown, tells me that his firm will also conduct property visits every three to six months to make sure that the tenant is properly looking after the unit. If the place is a mess, follow up visits are scheduled to make sure that the tenant properly looks after their own obligations.

All income and expense statements available online

Property Managers will typically collect all rents and pay some bills for the owner, usually property taxes and insurance. Most management companies have their own insurance policies that offer better rates and coverages than what an individual owner can negotiate in the market. The manager can then add the owner as an additional insured on the policy, making sure you have all the required coverage should anything happen. They will also ensure that the tenant takes out proper contents and liability coverage to protect the tenant as well. Landlords then have access on-line to these statements, which can be easily printed and given to their accountants for income tax preparation.

Managers believe in relationships

Managers are not exclusively on the landlord's side. If the tenants are happy, they look after the property better. That is why the main goal of property managers is to solve problems quickly, so both landlords and tenants are happy long term.

The cost is very reasonable

Brandon Sage, of Landlord Property & Rental Management Inc., www.landlord.net, tells me that for a little over $100 a month, an owner can enjoy the benefits of a professional manager. As Brandon says, if your time is worth at least $30 an hour, then for 4 hours each month, you can have peace of mind. Sharon Goldberg adds that for most investors, you do not think twice about trusting your stock portfolio to a professional manager. Why would you not do the same with your real estate properties.

It is not easy being a landlord. Using a professional manager will give you peace of mind and a safe investment over the long term.

Tenants can legally pay year's rent up front

By Mark Weisleder, Lawyer

Also found in the Toronto Star

A recent decision of the Ontario Superior Court should have a major impact on lease negotiations between landlords and tenants in Ontario. This could assist credit challenged tenants and tenants with pets from obtaining approval to their rental applications.

Here's what happened:

Alison Corvers agreed to rent a home from Tanveer Bumbi at 969 Mississauga Heights Dr. in Mississauga Ontario from May 1, 2013 to April 30, 2014 for $7,500 per month. Bumbi initially refused Corvers' rental application as a result of the fact that Corvers was from the UK, working in Ontario and was on a visitor's visa and Bumbi was concerned as to whether she would maintain the payments. Corvers then paid one years' rent in advance, being $90,000 to demonstrate her good faith. Bumbia accepted this. Corvers also paid a security deposit of $7,500 up front to cover potential damages to the unit.

The problem is that under Ontario's Residential Tenancies Act, a landlord cannot request more than first and last month's rent before a tenant moves into the property. The Act also states that anything in a lease that violates the Act is void. As such, after moving in, Corvers brought an application to court to pay the extra months' rent and the security deposit back to her, as she claimed that this was all demanded by the landlord. In an original decision dated October 7, 2013, Judge Kofi Barnes of the Superior Court of Ontario looked at a text sent by the tenant's real estate agent to the landlord's agent that said "Allison will pay 12 month's rent up front." Based on that, he decided that since the tenant offered the money up-front, it was legal. However, since the security deposit was not offered by the tenant, this amount had to be paid back.

The case was appealed and in a decision dated February 12, 2014, Superior Court judge Frank Marrocco agreed with Justice Barnes and explained that while a landlord could not "require" a tenant to pay more than first and last month's rent as a condition of the tenancy, if the tenant "offered" to pay more money in advance and the landlord accepted the payment, then it would be legal. In addition, the court held that interest on the entire prepayment of rent had to be paid by the landlord, in accordance with the rate prescribed under the Act, which was 2.5% in 2013 and .8% in 2014.

Lauren Sigal, a Toronto lawyer at Macdonald Sager Manis LLP who acted for the landlord on the case, tells me that both judges relied on a prior decision in 2009 of Royal Bank v Mcpherson in support of this position. In the Mcpherson case, the tenant prepaid a years' rent of $24,000 to the landlord and then the landlord lost the property to the bank after defaulting on his mortgage. The tenant said he did not owe any rent as he had prepaid it for a year. The bank argued that since the payment was illegal, it should not be binding. The court disagreed, and said that the bank must step into the shoes of the landlord and be bound by the prepayment. It would be unfair to penalize the tenant by not recognizing the prepayment.

As a result of the Mcpherson case, lenders who sell a rental property after an owner defaults will typically state that the buyer accepts any tenancy arrangement. A buyer in this situation must do due diligence in advance to try and verify what payments were made by the tenant to the prior landlord so that they are not faced with a similar situation where the tenant has prepaid rent to someone else and now they are stuck with it.

Here are the lessons to be learned from these cases:

- Landlords cannot advertise that they will require more than first and last month's rent in advance of the tenant moving in. This includes any security deposit.

- If the tenant offers to pay extra money up front, make sure that it is clear that the offer is coming from the tenant. This could include a deposit to cover any damages or clean the unit when the tenant wants to bring a pet.

- Tenants need to keep a receipt for the payment as proof that the amount was paid, in case it is ever challenged later by anyone.

Click here to read the article:

Be prepared when applying for any government tax rebate

by Mark Weiseleder, Lawyer.

Also found in the Toronto Star April, 2014

New home buyers and owners renovating their own homes continue to be confused about the GST/HST rebate.

There are different rules when you are moving into the home as your primary residence,

when you are renovating an existing home, or whether you intend to rent your new home as an investment property.

When you buy a new home or condominium and plan to make it your primary residence, the rebate is usually

included in the price. So if you paid $400,000, the real price including the tax is closer to $427,000.

In your agreement with the builder, you likely agreed to transfer your rebate to him,

bringing your price down to $400,000. If you do not move in on closing, you will have to pay the full amount.

If you decide to rent out your new home, you are still eligible for the HST rebate, under a different program,

called the HST new rental residential rebate.

If you substantially renovated your own home and paid the contractors yourself,

you may also be entitled to up to $16,000 in HST rebates. In all cases, you have up to two years from closing

your new home or completing your renovations to apply.

Figuring out what to do can be tough, says Michael Beallor of Rebate4U,

www.rebate4u.com a company that has helps homeowners collect the HST rebate.

He says it can be difficult for the average person to find their way through the Canada Revenue Agency and d

eliver the documents to support any claim for the HST rebate. Beallor says he's helped owners get $6 million in tax rebates. The company does not charge a fee up front, but collects when the rebate is paid. Another company that provide the same service is Custom Business Solutions at www.rentalrebate.ca. In addition, lawyers and accountants

also provide this service to their clients, as I do in my own law practice.

Some buyers intend to move in when they buy a condominium, but when it is ready years later, their circumstances have changed and so they sell. In these cases, the CRA typically says the buyers are no longer entitled to the HST rebate.

But there is a way to fight that, says Toronto author and tax lawyer David Sherman.

Sherman says if you can show that you intended to make the house or condo your primary residence,

but that circumstances changed, requiring you to sell, then you may be able to fight a reassessment.

You may have been relocated for work, there may have been a death in the family,

or a child may have intended to use the unit for university but then was accepted to a university out of town.

What is very important is that you have the right documents to support your claim when dealing with

the Canada Revenue Agency. You may need advice from a lawyer or accountant.

Speaking of rebates, my column of Feb. 28 was in part about first-time buyer rebates related

to the Ontario Land Transfer Tax. Scott Blodgett with the Ministry of Finance,

clarified an example used in the column which referred to a situation where a couple marry and buy a house.

One spouse has already claimed the rebate but sold the home before they got married and one

has never owned a house. Blodgett says the spouse who has never owned a home

can still claim 100 per cent of the land transfer tax rebate, even if they do

not take 100 per cent ownership of the property.

This also applies to the Toronto Land transfer Tax rebate.

If anyone has overpaid land transfer taxes, you have eighteen months to apply to the Ministry of Finance

for an overpayment.

Be prepared when applying for any tax rebate. Click here to read the article:

Friday, April 4, 2014

The Definitive Guide to Marketing Your Business Online

What a great on line book on optimizing your web strategy. it is a quick read wand well thought out. Take a look today to develop a winning social media strategy.

The Definitive Guide Link

The Definitive Guide Link

Monday, March 24, 2014

How the Internet chips away the MLS

Insight into the escalating war between Zillow and Move

What the Internet and Uber are doing to the taxi business is happening in its own way to real estate brokers and the MLS.

Earlier this month, Inman News reported from an industry conference that a study by Jonathan Green, vice president real estate services for CoreLogic (CLGX), found that nearly half of all homes sold last year were never listed in an MLS or were listed only after a buyer was lined up.

The MLS, that coveted and proprietary listing report that gave unique value and advantage to real estate agents using it for decades, is falling out of use in favor of more open, free listing services, such as Zillow (Z) and other off-MLS listings.

Inman reported that CoreLogic’s analysis compared public record transaction data with MLS data in four counties, and extrapolating on those findings shows that MLS use is rapidly declining.

Inman reported that Corelogic says that this raises significant questions for the industry:

Will the prevalence of off-MLS listings (or FSBOs) continue to grow?Will behavior change in proportion to inventory?Will brokers attempt to systematically or effectively monetize pre-MLS listings?Will this behavior dilute the “first position” status of the MLS as a marketing engine?Will this behavior change the perception of the MLS as the record of choice for listing and sales content?

What’s hurt the MLSs has been good for companies like Zillow. And Zillow has been aggressive in taking things to the next level as the company grows. Zillow’s website is an open listing for both real estate brokers and buyers.

In mid-March Move (MOVE) and the National Association of Realtors filed a lawsuit against Zillow and Errol Samuelson, chief industry development officer for Zillow, in a Washington state superior court, alleging breach of contract, breach of fiduciary duty and – most critically – misappropriation of trade secrets.

Samuelson was formerly president of Realtor.com and chief strategy officer of Move, Inc. Zillow also hired Curt Beardsley away from Move. Beardsley joined Zillow as vice president, industry development, responsible for building and strengthening Zillow's relationships with MLSs and other industry partners. Beardsley, 49, was most recently executive vice president of industry development of Move.

None of the parties will talk on the matter citing pending litigation, but Inman News scored an exclusive interview with Samuelson where he explained why he left Move to join Zillow.

Low Listing Inventory Continues

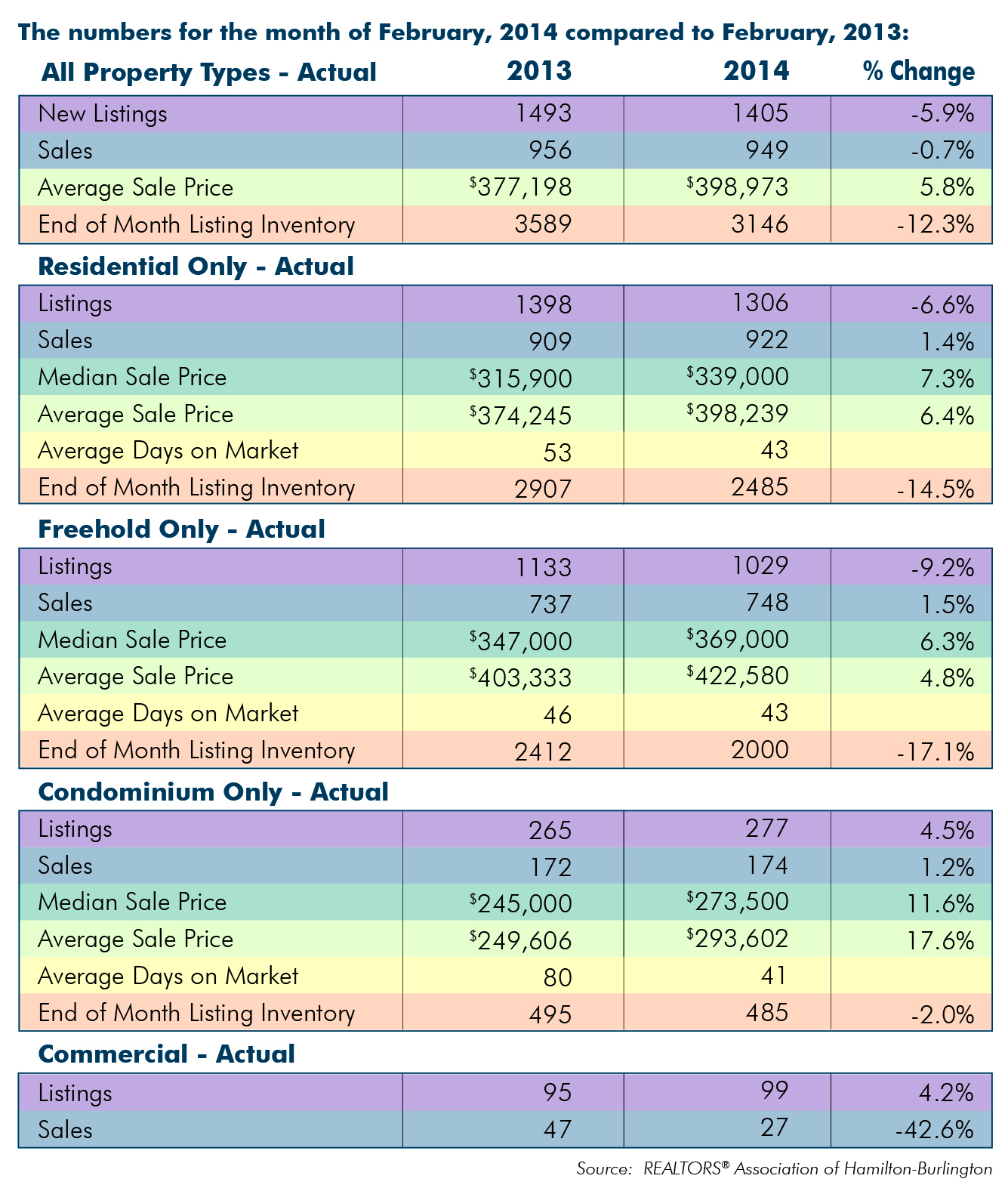

RAHB March 7, 2014 – Hamilton, Ontario) The REALTORS® Association of Hamilton-Burlington (RAHB) reported 949 property sales were processed through the RAHB Multiple Listing Service® (MLS®) system in February. This represents a 0.7 per cent decrease in sales compared to February of last year.

There were 1405 properties listed in February, a decrease of 5.9 per cent from the same month last year. End-of-month listing inventory was 12.3 per cent lower than last year at the same time.

The average sale price of $398,973 was 5.8 per cent higher than last February.

“The long winter seems to be having an effect on the real estate market,” said RAHB CEO Ross Godsoe. “Our listing inventory continues to be lower than average, and overall, for all property types, we are seeing fewer listings and sales compared to last year.”

Seasonally adjusted* sales of residential properties were less than one per cent higher than the same month last year, with the average sale price up 6.4 per cent for the month. Seasonally adjusted numbers of new listings were 5.4 per cent lower than the same month last year.

Seasonally adjusted data for residential properties for the month of February, 2014:

Actual overall residential sales were 1.4 per cent higher than the previous year at the same time. Residential freehold sales were 1.5 per cent higher than last year while the condominium market saw an increase of 1.2 per cent in sales. The average price of freehold properties showed an increase of 4.8 per cent over the same month last year; the average sale price in the condominium market increased 17.6 per cent when compared to the same period last year.

“Residential sales are up a bit from last year,” said RAHB CEO Ross Godsoe. “but when you look at the bigger picture, sales are actually almost seven per cent below what is average for the month of February, based on results from the last ten years. Likewise, listings are about 15 per cent lower than average.”

The average sale price is based on the total dollar volume of all properties sold. Average sale price information can be useful in establishing long term trends, but should not be used as an indicator that specific properties have increased or decreased in value.

The average days on market decreased from 46 to 43 days in the freehold market and from 80 to 41 days in the condominium market.

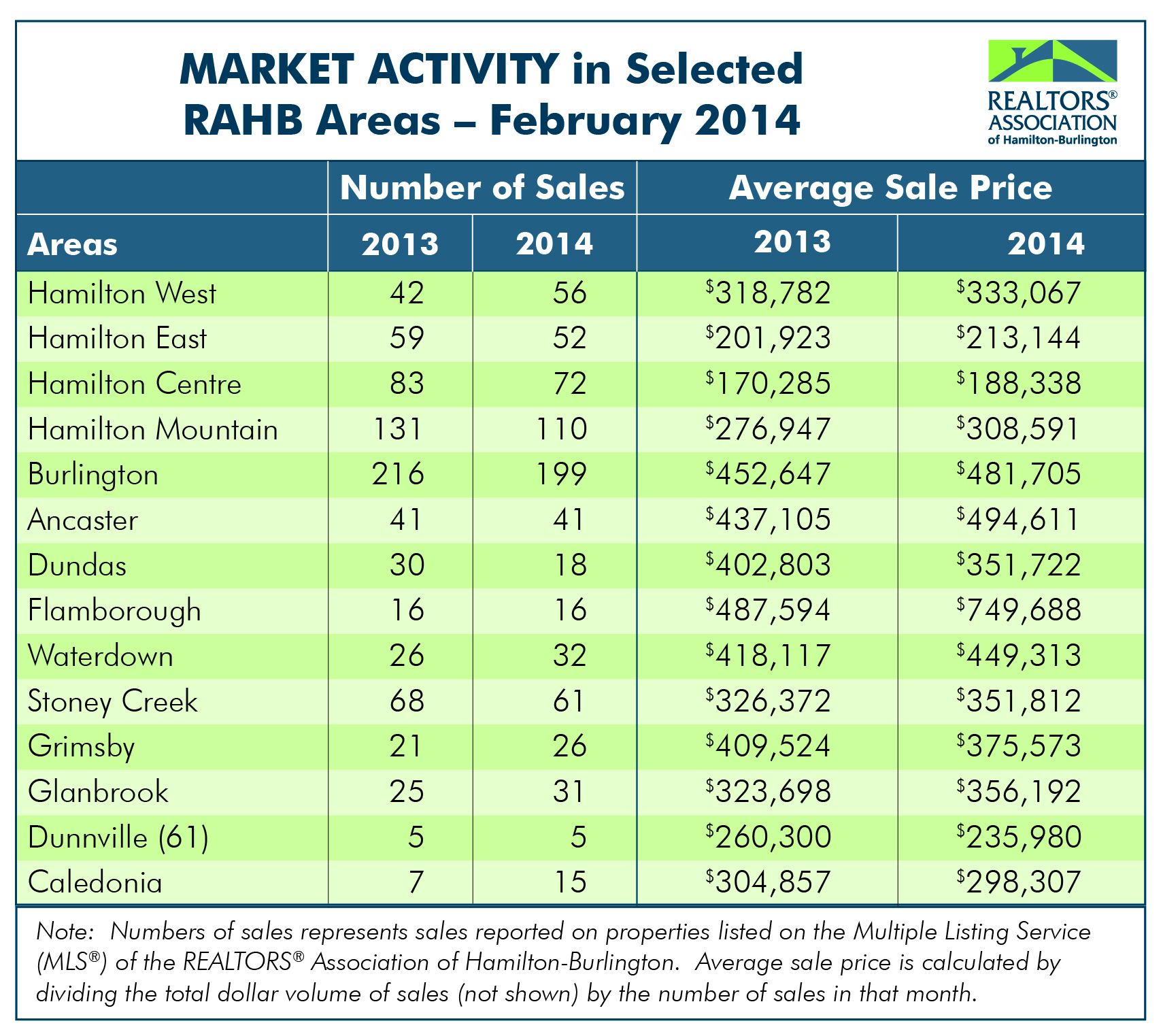

Every community in RAHB’s market area has its own localized residential market. Please refer to the accompanying chart for residential market activity in select areas in RAHB’s jurisdiction.

*Seasonal adjustment removes normal seasonal variations, enabling analysis of monthly changes and fundamental trends in the data.

Charm School for Real Estate Brokers BY CONSTANCE ROSENBLUM New York Times.

Sometimes it seems as if New York brokers can’t catch a break. The stereotype is that members of the species are rude, arrogant, aggressive, and more apt to talk than to listen. While the image may be just that — a stereotype — it clings to the people who help clients buy, sell and rent houses and apartments in this sharp-elbowed metropolis.

To counter this perception, many brokerages have professional coaches on staff; others bring in outside consultants. The goal is to teach brokers to project a warm and friendly image to their clients — who themselves aren’t always the easiest people in the world to deal with — and thus to be more effective in their work.

“For many years, the field of real estate didn’t change much,” said Laura Scott, an in-house coach with Douglas Elliman Real Estate, “and the broker was mostly an order-taker. But now, thanks to the Internet, everyone has his or her mousetrap, and so brokers have to be much more skilled, much smarter. They need to be better at building relationships, at getting out of their skin and putting themselves in their clients’ shoes, better at asking the right questions and not driving deals down people’s throats. That’s what we try to teach people to do.”Read Entire Article on New York Times

Friday, March 21, 2014

TREB Question? How do I get a history on a property through MPAC?

There has been much concern of late of he changes made by TREB to drop GEOWAREHOUSE in favour of MPAC for title search information. here is a quick link to the resource with MPAC to get a full history of a property form the time it was first developed.

TREB link

TREB link

Tuesday, March 18, 2014

A Manager by Any Other Name, Just Not Babysitter

Managing a real estate office is no easy thing, and unless you have a "specialist" that knows its nuances as your ally, you should evaluate the potential losses you haven't evaluated because of it.

I’ve heard it said that a manager at a real estate company is as useful as any of the fixtures one might find in such an office. This could be at a first glance, after all, if a manager is the most notable resource in a firm, it shouldn’t be for his/her hands-on participation, but for the results his effective administration ignites. In spite of what some may think about this key role, if you’re dealing with a trained, experienced professional, if you pay close attention, you just might hear the hum of that optimal operation. Forward thinking brokers forge ahead with a good lieutenant realizing that if nothing else, that person takes the brunt of the burdensome day to day responsibilities which would otherwise tie them up. What follows are some observations of how a manager achieves the best for all concerned, making him/her a most valued commodity in the process.

My first excursion into management at a real estate office was an eye opener, and a great springboard to launch a career. While I didn’t know it then, the role I thought was the epitome of achievement was a far cry from that, so far as the business owners were concerned. They underestimated the importance of this key person and thought it to be an unnecessary expense. And though they were averse to pay a good manager, they realized that if none of them invested their time managing the office, (or as they put it “babysit” the agents), they had to hire someone to do it, lest their business run amuck.

However, before getting ahead of myself, my immersion into this role came from a chance transaction with one of the principals at a local Century 21 franchise. In consummating that transaction the owner asked if I might be interested in a management position at his firm. After lots of discussions, a few group interviews, a thorough analysis of their situation and the existing staff, I was offered the position. This set into motion a course that would result in an unprecedented growth and productivity in just 12-months after assuming this charge.

Progress came at a rapid pace as a result of a careful orchestration and management of tasks, effort and time. Nevertheless, the improvements I initiated through a new operating procedures made my job that of monitoring systems and insuring they worked optimally, while maintaining high standards by means of simple checks and balances, and constant and specific training – on everything relevant to the strategies. As the staff and owners adapted to the changes, alliances were forged creating a cohesiveness that was unshakable – people rallied behind each campaign presented, and implemented innovation of their own, following one-on-one coaching. Adopting the mindset of “CANI,” popularized by Anthony Robbins in his 1986 book titled Unlimited Power, I modeled all aspects of the company’s culture around the philosophy of Constant And Never-ending Improvement, and the training I developed for the staff was progressive to that end. The company owners discovered how a good leader with a simple plan can achieve great things. Of course they loved the results – sales of over $36 million, with an average price of $150,000; more than 220 home sold, with a staff of 18 agents, an average of one house per agent per month! A true win-win-win situation.

To better appreciate how this unprecedented turnaround came about, keeping in mind that this 10-year old firm had up to this point never achieved this level of performance, let’s look at an excerpt from a little book I read a few years later -- Michael Berger’s The E-Myth, which emphasized five key principles, to achieving optimum results (in any business). What follows are those principles, which I used innately even before reading this excellent book:

Life: Your business is a way to get more out of your life. It is more than just a job you have created for yourself, but rather, it is there to serve you.

The Law of Objectivization: View your business as separate from you - as a product of you - and you will be able to reinvent it. It is about taking a step outside of your business, and looking at it objectively.

Working ON it not IN it: The business as a whole is the product, not the things or the services the business produces. You need to be focused on building your business, not merely cranking out products or services.

Systemization: View your business as an integrated system. The system does the work, and people run the system.

Business Development Cycle: The task of the owner is continuous development of the business through the ongoing process of innovation, quantification, and orchestration.

Essentially, my work mirrored these principles. In addition to being the conductor of the various tasks as noted above, one key function was to always be striving for greater accomplishments – through the staff and systems. Early on I adopted a tenet popularized by a phone company: “Telesis,” or progress intelligently planned, which reminded us of our focus.

Applying this principle, I participated in and graduated from NAR’s Council of Real Estate Broker Managers training that urged almost identical strategies…

- Develop effective sales associates who are aligned with the company’s culture.

- Identify and implement the critical elements of a learning program.

- Understand & adjust your leadership style based on the individual and the situation.

- Develop the skills necessary to coach, mentor and hold people accountable.

- Align your recruiting & retention strategy as part of the sales development process.

- Harness performance strategies to ensure agents will reach their full potential.

While this summary of my initiation is important in order to understand some of the steps to achieve a highly effective operation, it is but a backdrop to something a bit more comprehensive -- the question of when a brokerage ought to consider hiring a manager, and to what end.

Yes there is an added cost in hiring someone to do what you could do yourself, (sounds like the FSBO mentality to use a real estate axiom), but the benefits far outweigh them. After all, real estate is challenging, fraught with risks, inconsistent production, and turnstile-like approach to getting into the business, huge rewards, and extraordinarily successful performers; and while there is no cookie cutter formula for managing it all, so long as what you do is effective and simple enough to follow, it is all well and good. There are many factors that could make this job less time consuming or risky, but, there is little room to do it all or as thoroughly so as to avoid exposure and the high turnover rate.

Essentially the manager is a steward for the owner. S/he ensures that the owners vision, even if it were to only come in to collect a check, two or three weekly, is carried out with no significant strings attached (in reference to possible problems after the fact); in other words, risk management.

A manager’s primary role is to make it all work, and work well; profitably; seamlessly and consistently. As the leader, people will tend to follow the examples you set, and while a good producing agent sets a great example, such an agent typically isn’t the best choice for management – there just isn’t sufficient time to take someone under your wing without suffering setbacks in your own production. As the sales manager, you perform many roles. The key is to work on getting the most of all the resources and people, and to produce the best for the customer, all while keeping a tidy profit in the end.

If a manager is anything, s/he is certainly no babysitter. A manager is a most valuable resource, a commodity, an ally. And, as one risk manager commented at how this manager successfully diffused a tumultuous, high risk liability claim against the owner of another Century 21 franchise, by three attorneys vying for the same house, “…he is worth his weight in gold!” In other words, a true manager, someone with the temperance, patience and foresight to give his full commitment and do his best for your cause, is priceless, and a key person you will gladly want to invest in for all benefits and structure you, your staff and your customers will come to enjoy – a formula that leads to Telesis.

The Power of Showing Up

From Cracker Jack Agent

In many things in life, including business, to be successful you have to show up. In real estate, there's more to do than just show up, there's how you spend your time while your at it. Read on for tips on how you can make the most of your business time.

When I talk about "showing up" I am referring to being present in your business and really giving it your all. "Showing Up" means picking up the phone when you would rather send an email or doing an open house and connecting with people when you would rather be hiding in your office organizing your files. It is about stepping out of your comfort zone and connecting.

Believe it or not, "showing up" has nothing to do with the amount of time you put into your business. You could sit at your desk for eight hours but if all you have done during that time is send emails, scanned the MLS, poured a cup of coffee in the resource room, and chatted with the receptionist you may have put in your time, but you have not shown up. "Showing up" means putting on the show time attitude, connecting with people, and putting the best of you into your business.

I remember when I was a managing broker, managing an office with almost 80 agents. There were some agents who were in the office constantly. I assumed when I first came to the office that these were producing agents since they were in the office, ready for work. However, I was shocked to find out that some of these agents were not very productive with low sales numbers. You would have thought that all their "showing up" at the office would be paying off. But it wasn't paying off for them because while they were putting in time they were deluding themselves that their "busy work" tasks around the office would be effective in making their phone ring. They were not taking the extra step of "showing up" and making connections with their clients.

Then I met Sarah, a fairly new agent who was hardly ever in the office. Not only was she an agent, she was also juggling being a busy mother, wife, daughter, friend, and she even volunteered at her kids' school. Although I hardly ever saw her, she was bringing the best of herself to her business and connecting with others. Her results clearly reflected that. She had no choice but to use her time and energy efficiently and didn't waste with busy work. Because of how she was showing up in her business, she was one of the top agents in the office.

I remember a conversation she and I had discussing her schedule. She said she learned that her secret to success wasn't about just putting time in your business; it was about consistently doing the things that would bring results.

If you are one of those agents who may be putting in the hours but aren't seeing the results, take note. Many agents have discovered what Sarah has, but there are still those who struggle and tell themselves that they are working just because they are busy all day long. You may be spending way too much time on the computer, in your email, or even doing the laundry or playing with the dog at home during your best work hours.

Ask yourself if you are really bringing the BEST OF YOU to your job as CEO of your own company. A CEO's job is to motivate employees, usually with a focus on money-making activities. As the CEO of your own company, what review and direction would you give yourself as an employee?

Chances are if your business isn't where you want it to be, you need to be "showing up" more and putting the energy into connecting with others. If you connect well you will sell well.

If you need to take a close look at how you show up, I encourage you to write down all your activities for a week and color code everything you do for your business that includes showing up and connecting in green and code everything else in yellow. If you are not seeing a lot of green highlights, I guarantee you will not see a lot of green dollars.

Bring the best of you to the table, show up, and watch your business soar!

By Denise Lones CSP, M.I.R.M., CDEI - The founding partner of The Lones Group, Denise Lones, brings over two decades of experience in the real estate industry. With expertise in strategic marketing, business analysis, branding, new home project planning, product development, and agent/broker training, Denise is nationally recognized as the source for all things "real estate". With a passion for improvement, Denise has helped thousands of real estate agents, brokers, and managers build their business to unprecedented levels of success, while helping them maintain balance and quality of life.

Monday, March 17, 2014

Land Transfer Tax, Crack for Toronto Politicians

Is it fear or good management that makes us take action against items of concern. Sometimes I ponder this and come up with a tie. Good intentions, 1: Fear, 1.

This is something I ponder right now as I review the actions of all levels of government towards the real estate sector over the past five years. Let's look at those major factors one by one.

1. Land Transfer Taxes. In most of Ontario there is one Land Transfer Tax. In Toronto there are two.

We can argue why, or why not there should be two taxes, but one thing is certain, the second tax is costing Toronto buyers and sellers greatly.

When you review things as a percentage, it looks very small and unimportant. For simplicity, lets use 1% at the land transfer tax for Toronto and 1% for Ontario fully acknowledging the taxes are independently calculated by equations created by political hacks.

One percent is a very small thing as compared the an entire purchase price, the one hundred percent. When we look at it in actual dollars it is much more impactive. One percent (1%) is $5,000 of $500,000 purchases. For a $1,000,000 it is $10,000, sizeable indeed for most in Toronto.

But this is not the entire story. Let's add up the two Land Tramsfer Taxes and use a simple two percentage rate (2%). We now pay $10,000 on a $500,000 purchase and $20,000 on a $1,000,000 purchase! sizeable indeed. This is enough to buy a new compact car!

The question is, would this amount impact a buyer or sellers decision to enter the market place? Would a knowledgeable buyer or seller abort a potential transaction, or even not consider selling or buying simply because of this added cost. Invariably, the answer is yes, and the evidence is great that rational people have decided to not sell their current homes because of this unfair, duplicate taxation.

Really, states the doubting Thomas. Well, for many sellers, who would need to purchase a new, smaller property as they downsize, this added cost on the purchase will change their thoughts to hold on the their property rather than to pay the two taxes on their purchase. For some this may be a half year or more of wages, a sizeable sum definitely enough to make a decision on.

Remember, in the case of most who move, there are two transactions, the sale and the subsequent buy of a property. So although each transaction affords one tax times two (Ontario and Toronto taxes). in the overall scheme of things, moving from one home to the next in Toronto is impacted by something that resembles 4% of the overall transaction of one of the properties! Wow!

The Toronto Real Estate Board in the largest real estate MLS in North America. Evidence is clear that the Toronto real estate market place is impacted greatly as rational people refuse to enter the marketplace when they otherwise might simply sell or buy because the cost of entry has become too large. Sales volumes are down substantially compared to other neighbouring jurisdictions. Listing inventory is scarce at best and multiple offer bidding on properties is commonplace. What is frightfully noticeable however is the reduced inventory of homes for sale has caused a continuing and frightening price increase as rational buyers decide if they are to enter the market, they must pay more. Simple supply and demand theory at work, restrict the supply and the price will go up.

So the market is inflated by a tax that is duplicate even with all the best intentions.

I would argue that it is this Toronto specific tax that could be the straw that breaks the back of the Canadian real estate market. As Toronto goes, so goes Canada. So if this restrictive, duplicate tax continues, it could take down not only the Toronto real estate market, it could cripple the Ontario and Canadian market as the price of Toronto properties goes up even more.

One more thing, has anyone looked at what has happened to the absolute tax dollar paid per transaction over the last few years? Today the tax in real dollars is 70% higher than when started a short five years ago. So it contributes more to the Toronto tax base, and just like an injection of a hallucination, politicians refuse to even consider its removal or withdrawal. That happens with drugs, don't it! So maybe there are even more politicians on some sort of crack, land transfer crack!

This is something I ponder right now as I review the actions of all levels of government towards the real estate sector over the past five years. Let's look at those major factors one by one.

1. Land Transfer Taxes. In most of Ontario there is one Land Transfer Tax. In Toronto there are two.

We can argue why, or why not there should be two taxes, but one thing is certain, the second tax is costing Toronto buyers and sellers greatly.

When you review things as a percentage, it looks very small and unimportant. For simplicity, lets use 1% at the land transfer tax for Toronto and 1% for Ontario fully acknowledging the taxes are independently calculated by equations created by political hacks.

One percent is a very small thing as compared the an entire purchase price, the one hundred percent. When we look at it in actual dollars it is much more impactive. One percent (1%) is $5,000 of $500,000 purchases. For a $1,000,000 it is $10,000, sizeable indeed for most in Toronto.

But this is not the entire story. Let's add up the two Land Tramsfer Taxes and use a simple two percentage rate (2%). We now pay $10,000 on a $500,000 purchase and $20,000 on a $1,000,000 purchase! sizeable indeed. This is enough to buy a new compact car!

The question is, would this amount impact a buyer or sellers decision to enter the market place? Would a knowledgeable buyer or seller abort a potential transaction, or even not consider selling or buying simply because of this added cost. Invariably, the answer is yes, and the evidence is great that rational people have decided to not sell their current homes because of this unfair, duplicate taxation.

Really, states the doubting Thomas. Well, for many sellers, who would need to purchase a new, smaller property as they downsize, this added cost on the purchase will change their thoughts to hold on the their property rather than to pay the two taxes on their purchase. For some this may be a half year or more of wages, a sizeable sum definitely enough to make a decision on.

Remember, in the case of most who move, there are two transactions, the sale and the subsequent buy of a property. So although each transaction affords one tax times two (Ontario and Toronto taxes). in the overall scheme of things, moving from one home to the next in Toronto is impacted by something that resembles 4% of the overall transaction of one of the properties! Wow!

The Toronto Real Estate Board in the largest real estate MLS in North America. Evidence is clear that the Toronto real estate market place is impacted greatly as rational people refuse to enter the marketplace when they otherwise might simply sell or buy because the cost of entry has become too large. Sales volumes are down substantially compared to other neighbouring jurisdictions. Listing inventory is scarce at best and multiple offer bidding on properties is commonplace. What is frightfully noticeable however is the reduced inventory of homes for sale has caused a continuing and frightening price increase as rational buyers decide if they are to enter the market, they must pay more. Simple supply and demand theory at work, restrict the supply and the price will go up.

So the market is inflated by a tax that is duplicate even with all the best intentions.

I would argue that it is this Toronto specific tax that could be the straw that breaks the back of the Canadian real estate market. As Toronto goes, so goes Canada. So if this restrictive, duplicate tax continues, it could take down not only the Toronto real estate market, it could cripple the Ontario and Canadian market as the price of Toronto properties goes up even more.

One more thing, has anyone looked at what has happened to the absolute tax dollar paid per transaction over the last few years? Today the tax in real dollars is 70% higher than when started a short five years ago. So it contributes more to the Toronto tax base, and just like an injection of a hallucination, politicians refuse to even consider its removal or withdrawal. That happens with drugs, don't it! So maybe there are even more politicians on some sort of crack, land transfer crack!

Subscribe to:

Posts (Atom)